Livret A accounts – drowning in criticism

By Pierre Madec As the Governor of the Bank of France and the Minister of the Economy and Finance announced a further (probable) reduction in […]

By Pierre Madec As the Governor of the Bank of France and the Minister of the Economy and Finance announced a further (probable) reduction in […]

By Christine Rifflart The rise in public transport prices had barely been in force for two weeks when this lit the fire of revolt and […]

By Jean-Luc Gaffard The concept of a “vertical network” [filière] is back in the spotlight and is playing the role of an instrument of the […]

By Céline Antonin and Sandrine Levasseur On 1 July 2013, ten years after filing its application to join the European Union, Croatia will officially become […]

By Henri Sterdyniak Under pressure from the financial markets and Europe’s institutions, the government felt obliged to present a new pension reform in 2013. However, […]

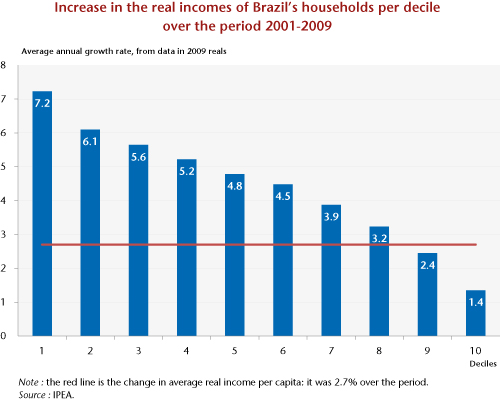

By Guillaume Allègre and Hélène Périvier As part of a review of family benefit programmes (the motivations for which are in any case debatable), the […]

By Céline Antonin, Christophe Blot, Sabine Le Bayon and Catherine Mathieu The crisis affecting the euro zone is the result of macroeconomic and financial imbalances […]

By Eric Heyer “France should copy Germany’s reforms to thrive”, Gerhard Schröder entitled an opinion piece in the Financial Times on 5 June 2013. As […]

By Christophe Blot and Fabien Labondance The transmission of monetary policy to economic activity and inflation takes place through various channels whose role and importance […]

By Mathieu Plane The figures for French growth for 2014 published by the European Commission (EC) in its last report in May 2013 appear to […]

Copyright © 2025 | WordPress Theme by MH Themes